In a puzzling stance, the European Union remains passive as a significant 21% of Russian liquefied natural gas (LNG) passes through its terminals to reach world markets, sparking concerns and discussions about the strategic choices and policies of member states.

The Zeebrugge terminal in Belgium has seen a staggering influx of LNG from Russia's Yamal region, nearly doubling the volume of direct Yamal LNG imports within the same period.

This surge is directly attributed to the Zeebrugge terminal's continued facilitation of transshipment services for Yamal LNG, an action that stands in stark contrast to the Netherlands' cessation of similar services and the UK's complete ban on Russian fuel imports.

There are reasons for concern about the growing role of Russia at LNG markets. According to Kpler data, Russian LNG exports to Europe were the highest ever in November 2023, totaling 1.75 million tons or 2.4 billion cubic meters. In November, Belgium received the largest volumes of Russian gas.

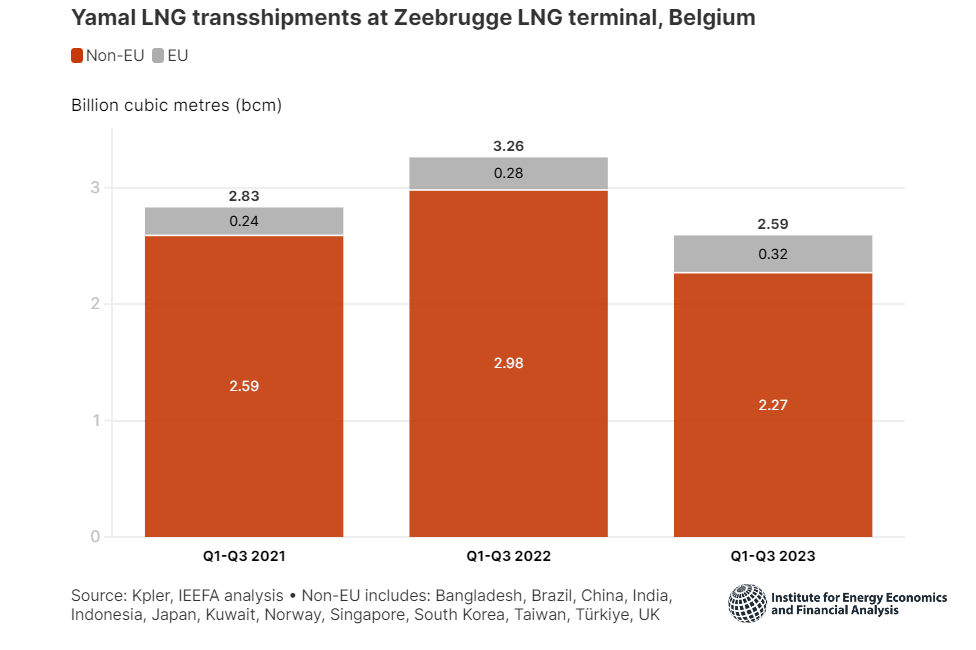

The analysis of shipment data performed by the Institute for Energy Economics and Financial Analysis (IEEFA) shows that approximately 90% of the transshipped Yamal LNG at Belgium's Zeebrugge since 2021 has been redirected to non-EU destinations, shedding light on the intricate dynamics of these operations.

Transshipments involve the intricate transfer of LNG between vessels, encompassing various methods like direct ship-to-ship transfers or the storage-based reloading process. Notably, Zeebrugge stands as the sole EU terminal that provides this service specifically for Yamal LNG cargoes.

Within commercial parameters, these transshipments often blur the lines between re-exports and official import figures.

The nuanced distinction sometimes leads to these actions not being accounted for in standard import statistics, despite their substantial impact on energy flows and trade balances.

Belgium's Fluxys secured a lengthy 20-year agreement with Yamal LNG for transshipment operations at Zeebrugge, marking a commitment of up to 8 million tonnes annually. The initiation of this agreement in 2019 was supported by Zeebrugge's infrastructure expansion to accommodate year-round deliveries to Asian markets.

Aside from Zeebrugge, the Montoir-de-Bretagne terminal partakes in a similar process, overseeing ship-to-ship transshipments of Yamal LNG.

This endeavor stems from a long-standing agreement between Engie, TotalEnergies, and Russian gas giant Novatek, facilitating the reception and transfer of 1 million tons of LNG from Yamal annually.

The transshipments conducted at Zeebrugge and Montoir-de-Bretagne are managed by Yamal LNG, using these European terminals as pivotal points for inter-vessel LNG transfers.

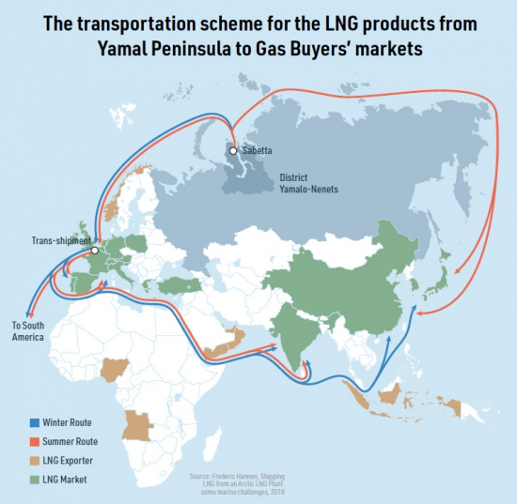

These operations are primarily intended to redirect LNG from icebreaker vessels departing from Russia's Sabetta terminal and navigating through Arctic waters during the November to June period, when passage via the Bering Strait to Asian markets becomes impassable due to icy conditions.

The EU's tacit allowance of such significant amounts of Russian LNG transshipments through its terminals raises pertinent questions about energy strategies, geopolitical allegiances, and the implications of these actions on the region's energy security landscape.

The shareholder landscape of Yamal LNG presents a mosaic of global influence and strategic alliances, with Russia's Novatek leading the consortium with a majority stake of 50.1%.

The collaborative essence is further highlighted by France's TotalEnergies holding a significant 20% share, while China National Petroleum Corporation (CNPC) and China's Silk Road Fund collectively possess a 29.9% stake.

A web of buyers, each with distinct volumes and commitments, reflects the diverse market outreach of Yamal LNG.

Notable purchasers include CNPC, securing 3 million tonnes per annum (mtpa), Gazprom Marketing & Trading with a steadfast commitment of 2.9 mtpa over a 20+ year period facilitated by the Zeebrugge transshipment nexus, Spain's Naturgy Energy Group at 2.5 mtpa, Novatek at 2.5 mtpa, and the robust commitment of TotalEnergies acquiring 4.0 mtpa.

The intricate dealings within LNG markets extend to portfolio players who engage in procurement from various global suppliers. Novatek, in particular, engages Gunvor with a purchase of 0.5 mtpa, while Shell and TotalEnergies collectively secure 1.9 mtpa, sourced from Yamal and orchestrated via transshipment at Montoir-de-Bretagne.

Recent assessments of Yamal LNG's traffic and trade reveal compelling insights into the transshipment dynamics.

The volumes dispatched to Montoir-de-Bretagne during the first three quarters of 2023 surpassed reported import figures by a staggering 50%, primarily attributable to redirections to other nations.

Notably, approximately 76% of the transshipped Yamal LNG from Montoir-de-Bretagne in 2023 is earmarked for non-EU destinations, marking a substantial surge from the 50% recorded in 2021.

Belgium and France, key recipients of Russian LNG, received 6.32 billion cubic meters (bcm) from Yamal during the same period.

However, an additional 3.78 bcm of Yamal LNG was rerouted to their terminals for subsequent transshipment to other nations or internal terminals. This practice entails rerouting 37% of Russian LNG received by these countries for various international or domestic purposes.

Notably, the aggregated flow of LNG from Russia's Yamal, Vysotsk, and Portovaya terminals amassed to 17.77 bcm between January and September 2023.

Intriguingly, approximately 21% of all Russian LNG channeled to the EU involves transshipments, signaling a lingering presence of Russian LNG within EU ports even beyond 2027.

This timeline aligns with the EU's ambitious goal of achieving autonomy from Russian fossil fuel imports through the REPowerEU initiative, highlighting the region's complex interplay of energy geopolitics and strategic goals.